Backtesting

Backtesting lets you run a strategy against historical price data to see how it would have performed in the past. It's the fastest way to validate your trading logic before risking any money.

Running a backtest

- Open the Backtesting panel in the right sidebar

- Click New Backtest

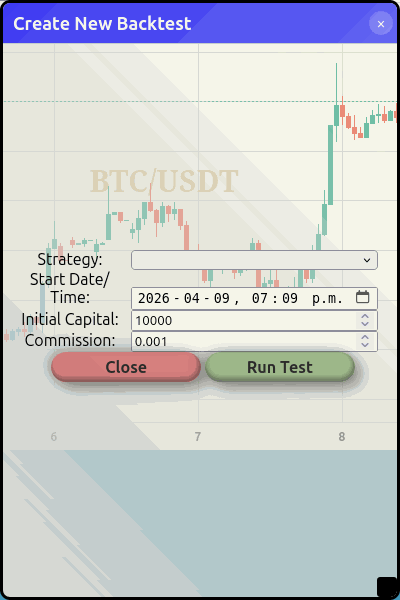

- Configure the backtest:

Set your strategy, date range, starting capital, and commission rate

Set your strategy, date range, starting capital, and commission rate

- Strategy — Select which strategy to test

- Start date — How far back to test from

- Initial capital — Starting balance (default: $10,000)

- Commission — Trading fee percentage (default: 0.1%)

- Click Run Test

The backtest runs your strategy tick-by-tick through the historical data. Depending on the timeframe and date range, this can take a few seconds to a minute.

Interpreting results

After the backtest completes, you'll see:

- Total return — How much your initial capital grew (or shrank)

- Trade list — Every trade the strategy made, with entry/exit prices and P/L

- Equity curve — A chart showing how your portfolio value changed over time

Tips for better backtests

warning

Past performance does not predict future results. A backtest shows what would have happened, not what will happen. Always paper trade before going live.

- Test across different market conditions — A strategy that works in a bull market may fail in a sideways or bear market. Test across different date ranges.

- Watch for overfitting — If your strategy has many parameters tuned to a specific period, it may not generalise well. Keep it simple.

- Account for commission — The default 0.1% commission is typical for major exchanges. Adjust if your exchange charges differently.

- Check the trade count — A strategy that made 3 trades over a year isn't enough data to be confident. Look for strategies with a meaningful number of trades.